How to Avoid the Debt Trap as an International Student in Australia?

The idea is that other people’s mistakes and successes can teach you whether you should behave the same way, or differently.

So in this article, I will give tips to avoid the debt trap as an international student in Australia.

Avoid Credit Cards / Buy Now Pay Later Offers

It’s spending money that you don’t have yet. It is very lucrative to buy the latest gadgets and think that you will pay easily in installments but as an international student unexpected things can happen.

If you miss one of those installments, these companies and services will start charging you interest rates and late fees and that’s how the cycle of debt trap starts, and it just keeps on growing, and you feel trapped and helpless. That latest $1000 smartphone can cost you double the amount plus your lost sleep and mental health.

Keep in mind that if you are unable to pay and considered as a defaulter, it will affect your credit score, which can ultimately affect your borrowing capacity.

Buy Now, Pay Later vs. Credit Cards

Understand Your Finances

Check where your money is going and where it is coming from. Create a budget on a spreadsheet, write on paper or whatever is easier for you.

It will give you an exact idea of how much you are spending and how much you are earning and importantly, how much money you are saving.

Keeping Budget in Control

When your income increases, don’t increase your expenses. Use your spreadsheet that was made earlier and keep a regular check of expenses, earnings and savings. I would suggest that you should update your spreadsheet at least once a month.

If you aren’t sure, then I recommend you check the Australian Government’s Moneysmart website, which talks about how to create a budget for yourself.

Create an Emergency Funds

Financial experts recommend that you keep at least 3 months’ worth of expenses, but you can start from $1000 or start building up your emergency funds any time you can. But this fund is only for Emergencies like paying excess for insurance.

Save for an emergency fund – Moneysmart.gov.au

Learn Finance

Everyday Finance should be taught in schools but unfortunately, it’s not. Everyone should learn everyday Finance as soon as they can. You don’t have to be a financial wizard but you should know the basics about your money so you can get its worth.

You should have a basic knowledge of budgeting, saving, taxation and how to keep your money safe. Here’s one book recommendation to start with – The Barefoot Investor by Scott Pape.

I also encourage you to do your own research on YouTube and Google.

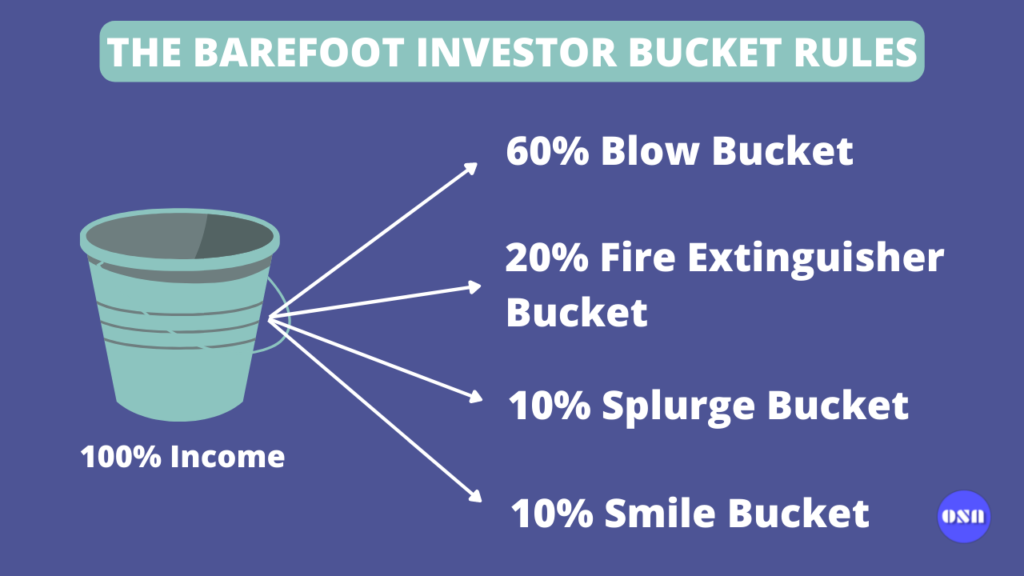

Barefoot Investor Rules

Here’s one of the core basics from the book. The book makes setting up the buckets easy for you, but basically, this is how you should be allocating your income each time you get the paycheck:

- 60% to your Blow Bucket. (This is your everyday expenses)

- 20% to your Fire Extinguisher Bucket. (This is to pay for your debt)

- 10% to your Splurge Bucket. (This is to spend on yourself, like buying new shoes or treating yourself)

- 10% to your Smile Bucket (This is your long-term savings account)

Important Resources for getting help

National Debt Helpline:

1800 007 007. If you are already suffering from the debt I would highly recommend you to call and get FREE information and advice. You can get help from this helpline even if you are an international student in Australia.

Moneysmart: – Visit this website (https://moneysmart.gov.au/ ) to find tools and information for your journey.

Please note that this is not financial advice, the information presented here is based on personal life experiences of the author.

Always do your own research and cross-check information as the information might change or improve as time passes. If needed, please seek professional advice.

Article written by: Gursewak Singh

Gursewak is an ex-international student living in Newcastle, Australia. When he is not working, he likes to do photography. His favourite food is Pancakes.

You can reach out to him via Instagram @sidhu.au